Executive Summary

Convolutional Neural Networks, usually called CNNs, are one of the most important architectures in the history of modern artificial intelligence. They changed computer vision, enabled breakthroughs in document recognition, image classification, object detection and segmentation, and became a foundation for many deep learning systems used in industry.

For banks, however, the real question is not whether a Convolutional Neural Network is technically impressive. The real question is whether it is appropriate for the use case, whether the bank understands what the model is learning, whether the data is controlled, whether the output can be explained sufficiently, and whether the model can be governed under banking regulation.

That is where CNNs become strategically relevant.

In banking, CNNs may appear in fraud detection, document processing, KYC workflows, signature verification, cheque recognition, invoice analysis, anomaly detection, transaction-pattern analysis and visual or image-like representations of financial data. But once a CNN touches customer outcomes, financial crime controls, credit processes, operational resilience or regulatory reporting, it stops being only a data science topic. It becomes a model risk, data governance, operational resilience and accountability topic.

This article is not a technical tutorial. It is a banking technology and governance perspective on Convolutional Neural Networks: what they are, where they matter, why they are not always the right answer, and what boards, CIOs, CROs and AI governance functions should ask before deploying them in a supervised institution.

What Is a Convolutional Neural Network?

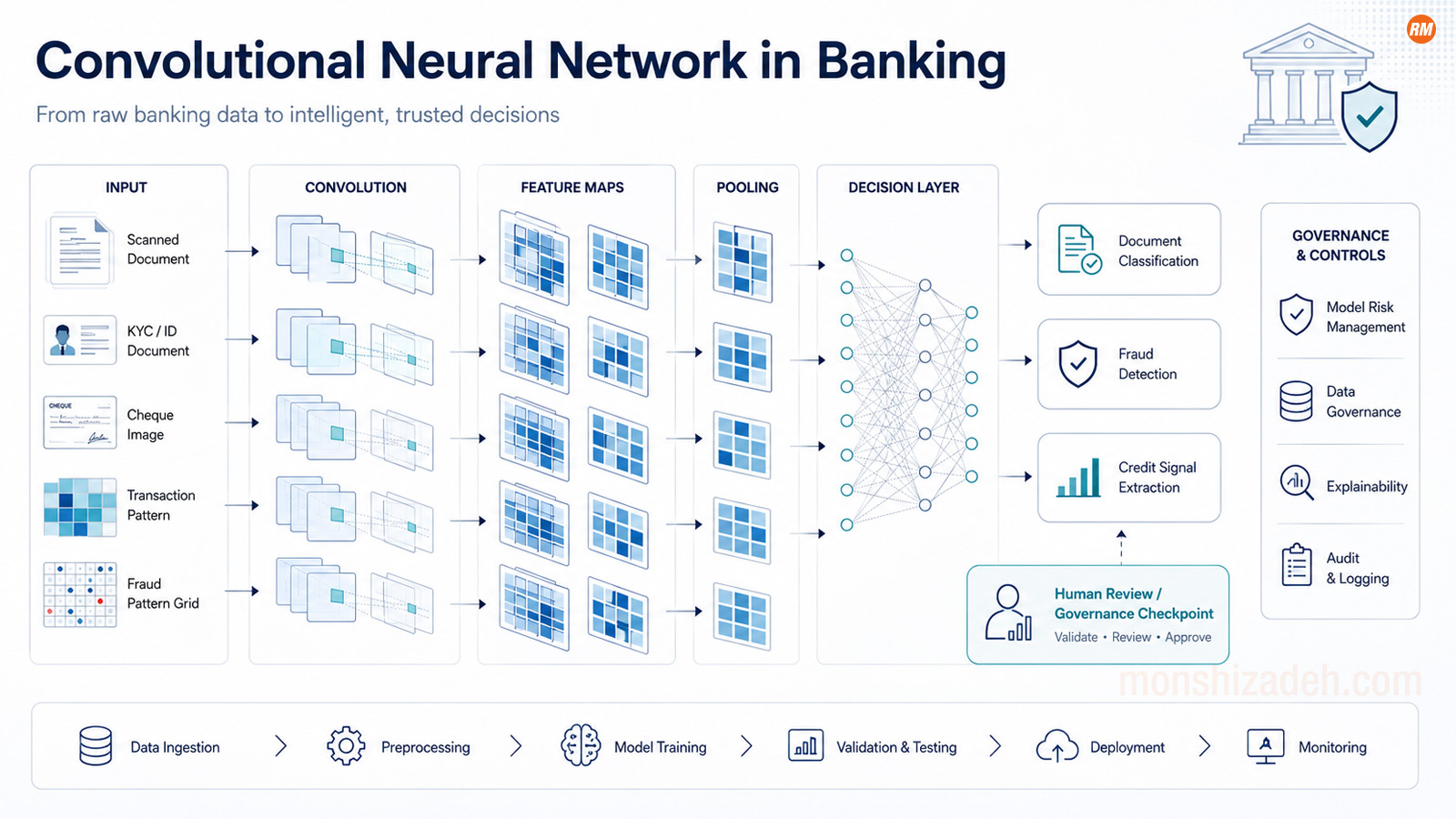

A Convolutional Neural Network is a type of neural network designed to detect patterns in structured data, especially data with local relationships. In images, for example, nearby pixels matter. A CNN learns filters that detect edges, shapes, textures, objects and eventually higher-level patterns. Instead of treating every input feature as fully independent, CNNs exploit structure.

That is why CNNs became so powerful in computer vision.

The roots go back decades. LeCun, Bottou, Bengio and Haffner’s 1998 paper on gradient-based learning for document recognition presented LeNet-5, one of the canonical CNN architectures, and demonstrated CNN-based recognition of handwritten characters and documents. That historical link to document recognition is important for banking because banks have always processed documents, forms, cheques, signatures and structured records at scale. (ieeexplore.ieee.org)

The modern deep learning era accelerated after AlexNet. In 2012, Krizhevsky, Sutskever and Hinton trained a large deep CNN on ImageNet and achieved a breakthrough in large-scale image classification. That result is widely viewed as one of the decisive moments that pushed deep learning into mainstream industrial AI. (proceedings.neurips.cc)

After that, CNN architectures evolved quickly: VGG, Inception, ResNet, DenseNet, Xception, MobileNet, EfficientNet and others. ResNet, for example, introduced residual learning to make very deep neural networks easier to train and won major ImageNet and COCO tasks in 2015. (arxiv.org)

But the technical history is not the point for a bank.

The point is this: CNNs are powerful pattern-recognition systems. And in banking, pattern recognition is valuable only when it is connected to control, evidence and accountability.

Why CNNs Matter in Banking

CNNs are most naturally associated with image recognition, but their relevance in banking is broader.

The most obvious application is document intelligence. Banks process passports, IDs, invoices, statements, contracts, tax documents, account-opening forms, signatures, cheques and regulatory evidence. A CNN-based model can help classify documents, extract visual features, detect inconsistencies or support optical character recognition workflows.

A second area is fraud detection. Financial fraud often appears as a pattern problem: abnormal transaction sequences, unusual customer behaviour, inconsistent merchant patterns, manipulated documents, synthetic identities or suspicious visual evidence. CNNs may be used directly on image data, or indirectly when transaction data is transformed into image-like or matrix-like structures.

A 2025 systematic review of deep learning in financial fraud detection examined 108 peer-reviewed publications from 2019 to 2024 and identified CNNs, LSTMs, transformers and ensemble methods across domains including credit cards, insurance and financial reporting. The important conclusion for banks is not that CNNs are always superior. The conclusion is that deep learning architectures are increasingly part of the fraud-detection toolkit, and that governance must be able to deal with them. (sciencedirect.com)

A third area is KYC and onboarding. CNNs can support image-based checks, document classification, visual anomaly detection and identity-verification workflows. But this is also where risk increases quickly. If the model affects customer onboarding, access to banking services or financial crime controls, the bank must be able to evidence how the model works, how it is monitored, what data it uses and how errors are handled.

A fourth area is operational risk and cyber. CNNs and related deep learning approaches can be used for pattern recognition in logs, alerts, screenshots, behavioural signals or anomaly detection. But again, the question is not only whether the model detects patterns. The question is whether the bank can rely on it in a controlled environment.

This is the strategic lesson: CNNs are useful where the data has structure. They are less convincing when used only because “deep learning” sounds advanced.

In banking, the model architecture should follow the risk problem. Not the other way around.

The Board-Level Misunderstanding

Boards and senior executives rarely need to understand convolution kernels, pooling layers or activation maps in technical detail. But they do need to understand what kind of governance question a CNN creates.

A CNN is not just a model. It is a decision-support mechanism embedded into a process.

That process may involve customer data, financial crime detection, operational risk, third-party technology, cloud infrastructure, manual review, escalation paths and audit evidence. If the model performs poorly, the consequences may include false positives, false negatives, customer harm, missed fraud, operational backlog, regulatory concern or over-reliance on an opaque system.

The wrong board question is:

“How advanced is the model?”

The better question is:

“What decision does this model influence, and can management evidence control over that decision?”

That is the shift from technology curiosity to governance maturity.

A CNN used to classify internal scanned documents may be relatively low risk. A CNN used to support fraud detection or customer onboarding may be materially more sensitive. A CNN used in a credit-related workflow could become highly significant, depending on the use case and decision impact. Under the EU AI Act, AI systems used to evaluate the creditworthiness of natural persons or establish their credit score are classified as high-risk, with an exception for AI systems used to detect financial fraud. That distinction matters because it shows that classification depends on purpose, not only on technology. (ai-act-service-desk.ec.europa.eu)

A bank therefore cannot govern CNNs by asking only, “What architecture is this?”

It must ask:

“What is the system used for?”

That is where banking governance begins.

Why CNNs Are Not Always the Right Model

A serious AI strategy should avoid architecture fashion.

CNNs are powerful when the data structure fits the model. They work well for images, spatial patterns, local feature relationships and some transformed representations of sequential or tabular data. But many banking datasets are tabular, relational, sparse, time-dependent or network-based. In those cases, other model families may be more appropriate: gradient boosting, graph neural networks, recurrent architectures, transformers, anomaly-detection methods, rule-based systems or simpler statistical models.

This matters for governance because model complexity must be justified.

A bank should not accept a CNN simply because a vendor claims it is “deep learning”. The bank should ask why a CNN is appropriate for the use case, what baseline model it was compared against, whether simpler models performed adequately, what performance metric matters, and whether the added complexity is worth the governance burden.

In fraud detection, for example, accuracy alone can be misleading. Fraud datasets are often highly imbalanced. A model can look accurate while missing the events that matter. Precision, recall, false-positive rate, false-negative rate, operational workload, customer friction and investigation capacity may matter more than headline accuracy.

This is a classic banking point: a model is not good because it scores well in a lab. It is good if it improves a controlled business process under real operating conditions.

A CNN that increases fraud detection but overwhelms investigators with false positives may not be a good model. A CNN that improves document classification but cannot be monitored for drift may create operational risk. A CNN that works in one country but fails across languages, document formats or customer groups may create fairness, conduct and control issues.

Model performance is only one part of model governance.

Explainability: The CNN Governance Problem

CNNs are often treated as black-box systems because their internal representations are difficult to interpret. That does not mean they cannot be governed. It means the governance model must define what level of explanation is necessary for the use case.

Explainability depends on audience and purpose.

A data scientist may need technical diagnostics. A model validator may need sensitivity analysis, feature behaviour, robustness testing and failure modes. A business owner may need to know when the model should be trusted and when it should be escalated. An investigator may need visual or operational reason codes. A supervisor may need evidence that the bank understands the model’s limitations and controls them.

Grad-CAM is one important method in the CNN explainability literature. Selvaraju and co-authors proposed Grad-CAM to produce visual explanations for decisions from CNN-based models by highlighting regions of an image that are important for a model’s prediction. In banking, that type of technique may be useful when reviewing document-classification models, image-based verification tools or other visual AI systems. (arxiv.org)

But explainability tools are not magic.

A heatmap is not governance. A saliency map is not accountability. A visual explanation can help, but it does not prove that the model is fair, robust, stable, lawful or appropriate for the use case. It must be part of a broader evidence package: data lineage, validation, performance testing, bias assessment, monitoring, override analysis, incident handling and audit trail.

This is where banks need discipline.

The right question is not: “Can we explain every neuron?”

The right question is: “Can we explain the model sufficiently for the decision it supports, the risk it creates and the person or function relying on it?”

That is a practical explainability standard.

Adversarial Risk and Robustness

CNNs also introduced one of the most important lessons in modern AI risk: models can be highly accurate and still fragile.

Szegedy and co-authors showed that neural networks can be vulnerable to adversarial examples — small input changes that can cause incorrect classifications. This finding matters far beyond academic computer vision. It shows that model robustness cannot be assumed from average performance alone. (arxiv.org)

For banks, this is especially relevant in adversarial environments.

Fraudsters adapt. Criminal networks test controls. Document manipulation evolves. Synthetic identities become more sophisticated. Cyber attackers probe systems. If a CNN is used in fraud detection, document verification or onboarding, the bank should assume that adversarial pressure may exist.

That changes the validation standard.

A bank should test not only whether the CNN works on historical data, but whether it remains robust under manipulated, degraded, noisy, incomplete, shifted or adversarial inputs. It should test performance across customer groups, geographies, channels, document types, device quality and time periods.

The model should also be monitored after deployment. CNN performance can degrade when data changes. New document templates, new fraud typologies, new imaging conditions, new customer behaviour or vendor model updates can shift the input distribution.

This is where monitoring becomes governance.

If the model changes, or the world changes around the model, the bank must know.

CNNs, DORA and Third-Party Risk

CNN governance cannot be separated from technology governance.

Many CNN-based capabilities will not be built entirely inside the bank. They may come through vendors, cloud AI platforms, document-processing tools, fraud analytics providers, onboarding platforms, data providers or external model APIs. Under DORA, financial entities must manage ICT risk and ICT third-party risk as part of digital operational resilience. DORA also establishes an EU-wide oversight framework for critical ICT third-party providers. (eiopa.europa.eu)

That matters directly for CNNs.

If a bank uses a vendor model for document classification, who controls the model version? Can the bank test it independently? Can the bank restrict data use? Can it prevent the vendor from using bank data for training? Are logs retained? Is the model hosted in a controlled environment? Is there an exit plan? What happens if the vendor changes the model? What happens if the service is unavailable? What happens if performance deteriorates?

These are not technical details. They are governance questions.

A CNN embedded in a vendor product is still part of the bank’s control environment if it affects banking processes. The fact that the model is hidden inside a third-party tool does not remove the bank’s accountability.

This is a common failure mode. A business team buys a document-processing platform. The platform includes AI. A new feature is activated. Data begins to flow. Outputs enter a workflow. The AI inventory is not updated. Risk classification is not revisited. The control function sees it too late.

That is how embedded AI becomes unmanaged AI.

For a bank, the safest assumption is simple: if a vendor tool uses AI and affects a banking process, it belongs in the AI inventory.

The EU AI Act Lens: Purpose Beats Architecture

One of the most important lessons from the EU AI Act is that governance classification is use-case driven.

The same CNN architecture can create different governance obligations depending on its purpose.

A CNN used to classify internal training images may be low risk. A CNN used to verify identity documents may raise data protection, fraud and onboarding-control questions. A CNN used in a creditworthiness workflow may become materially sensitive. A CNN used for detecting financial fraud may be governed differently from a CNN used to evaluate creditworthiness, even if the technical architecture looks similar.

That is why banks should not classify AI systems by architecture alone.

They should classify by purpose, decision impact, affected population, data sensitivity, regulatory relevance, operational dependency and third-party exposure.

This also matters for documentation. A model card that describes technical performance is not enough. The bank needs a use-case record: business purpose, decision role, process owner, data owner, model owner, validation status, monitoring approach, human oversight design, incident triggers, regulatory classification and retirement criteria.

The AI Act should therefore be treated as a governance trigger. It forces a bank to ask a better question: not “what model are we using?” but “what role does this system play in a regulated decision environment?”

That question is more important than the architecture.

The CNN Inventory: What a Bank Should Capture

If a bank uses CNNs, it should not rely on scattered documentation.

It needs an inventory view.

At minimum, the AI or model inventory should capture:

* model name and architecture family; * business process and legal entity; * use-case owner and model owner; * internal or third-party development source; * data sources and data rights; * personal data involvement; * customer or employee impact; * decision role: advisory, prioritisation, automation or control; * regulatory relevance; * EU AI Act classification; * DORA and outsourcing relevance; * validation status; * explainability method; * monitoring metrics; * drift indicators; * override process; * incidents and issues; * retirement or kill criteria.

This may sound administrative. It is not. Without this inventory, management cannot know where CNNs are used, what they influence, who owns them and whether they are controlled.

The inventory is the bridge between data science and executive accountability.

For a Head of Governance, Head of Technology, CIO, CRO or board member, the inventory is often more important than the model architecture. The architecture explains how the model works. The inventory explains whether the bank controls it.

Human Oversight and CNN Output

CNNs often produce scores, classifications, labels, bounding boxes, segmentations or visual explanations. In a banking process, those outputs frequently go to humans: investigators, operations teams, onboarding analysts, fraud specialists, credit officers, compliance teams or customer service agents.

The governance question is whether those humans can meaningfully challenge the model.

Human oversight is not meaningful simply because a person is present. The human reviewer needs competence, authority, time and escalation rights. They need to know when the model is reliable, when it is uncertain, when outputs should be overridden and when issues should be escalated.

This is particularly important where CNN outputs look visually persuasive. A heatmap, document label or fraud score may create confidence. But confidence is not correctness.

Banks should therefore monitor overrides. If humans frequently override a CNN, the model may be weak, the threshold may be wrong, the process may be unclear or the human team may not trust the system. If humans never override the model, that may also be a warning sign. It may indicate automation bias or rubber-stamping.

Human oversight must be observable.

A bank should be able to answer: who reviewed the output, what they saw, what they decided, whether they challenged the model, and what happened next.

That is not bureaucracy. That is evidence.

CNNs After the Transformer Shift

CNNs are no longer the only dominant architecture for vision tasks.

Vision Transformers challenged the idea that convolution was always necessary for image recognition. Dosovitskiy and co-authors showed that a pure transformer applied to image patches could perform strongly on image classification when trained at scale. (arxiv.org)

At the same time, CNNs did not disappear. ConvNeXt re-examined ConvNet design in the transformer era and showed that modernised convolutional networks can remain competitive on vision tasks while preserving the simplicity and efficiency of standard ConvNets. (arxiv.org)

For banks, this has a simple implication: architecture choice will keep changing.

The governance model must be stable enough to handle CNNs, transformers, hybrid models, graph models and future architectures. A bank should not build governance around one model class. It should build governance around use case, impact, data, control, accountability and evidence.

That is why CNNs are a good entry point for a broader conversation. They are historically important, still practically relevant and governance-heavy enough to show the real problem.

The problem is not CNNs.

The problem is whether banks can govern complex AI models before they become uncontrolled dependencies.

What Boards Should Ask

Boards do not need to discuss convolution filters. They do need to ask the right governance questions.

They should ask:

- Where are CNNs or similar deep learning models used in the bank today?

- Are they used in document processing, onboarding, fraud detection, financial crime controls, credit processes, operations or regulatory reporting?

- Which of these models affect customer outcomes, operational decisions or control processes?

- Are any of the models embedded in vendor tools?

- Who owns each model end to end?

- What data was used to train and validate the model?

- Can management evidence that data use is lawful, controlled and appropriate?

- How was the model validated against simpler baselines?

- What explainability method is used, and for whom?

- How are false positives and false negatives monitored?

- Can human reviewers override the model, and are overrides analysed?

- How is model drift detected?

- What happens if the vendor changes the model?

- Is there an exit plan?

- What is the business value, and what are the kill criteria?

These questions separate serious AI adoption from technology theatre.

Conclusion: CNNs Are a Test of AI Governance Maturity

Convolutional Neural Networks deserve their place in AI history. They shaped modern computer vision, transformed document recognition, enabled large-scale image classification and influenced many applied AI systems used today.

But in banking, technical importance is not enough.

A CNN used in a supervised institution must be governed through the same lens as any material AI capability: purpose, data, model risk, explainability, operational resilience, third-party dependency, human oversight, monitoring and accountability.

The wrong conclusion is that every bank needs more CNNs.

The right conclusion is that every bank needs the ability to govern advanced models when they appear inside banking processes.

Some CNN use cases will create real value. They may improve document processing, fraud detection, onboarding, operational efficiency or control effectiveness. Some will not. Some will add complexity without improving outcomes. Some will be better solved by simpler models. Some will create risks that outweigh their benefits.

That is why model governance must include business value, not only model performance.

A bank with many advanced models and weak governance is not technologically mature. It is exposed.

A bank with fewer models, better inventories, clearer ownership, stronger validation, controlled data, explainable outputs, monitored performance and real kill criteria is in a stronger position.

Convolutional Neural Networks are therefore not just an AI topic. In banking, they are a governance topic.

The decisive question is not whether the bank understands CNNs as a technology.

The decisive question is whether the bank can evidence control over the decisions, processes and risks that CNNs influence.

======= SEO title: Convolutional Neural Networks in Banking: From Pattern Recognition to Model Risk Governance

Meta description: A board-level perspective on Convolutional Neural Networks in banking, covering fraud detection, document processing, explainability, EU AI Act classification, DORA, third-party risk and model governance.

Primary keywords: convolutional neural network, convolutional neural networks in banking, CNN in banking, AI governance, model risk management, fraud detection, document processing, explainability, Grad-CAM, EU AI Act, DORA, third-party AI, AI in banking.

Add to all links: ?utm_source=monshizadeh.com