Executive Summary

Artificial intelligence is no longer difficult to access. The difficult part is proving where it creates measurable business value.

That distinction matters. A bank can deploy generative AI assistants, machine learning models, document intelligence, fraud analytics, software-development copilots or knowledge-management tools. But deployment is not value. Usage is not value. A pilot is not value. A model output is not value.

AI business value becomes real only when a measurable business outcome changes.

That outcome may be faster processing, lower rework, better risk detection, improved customer experience, reduced operational loss, higher straight-through processing, better software delivery, stronger knowledge reuse, improved control effectiveness or more scalable decision support. But each outcome needs a baseline, an owner, a value hypothesis, a measurement method and a decision rule.

The evidence is encouraging, but it is also highly context-specific. Task-level experiments show material productivity gains in writing, customer support and software development. Other studies show that AI can also underperform in specific expert settings or create uneven effects across tasks. That is why AI value measurement must be disciplined, not promotional.

For banks, this is the right framing. The relevant question is not “How many AI use cases do we have?” The better question is: “Which AI use cases have changed a measurable business outcome, and can we evidence the causal path from model output to enterprise value?”

That is what this article addresses: how to measure AI business value in a way that is useful for boards, executives, Finance, Technology, Risk, control functions and business owners.

Why AI Business Value Is Hard to Measure

AI value is difficult to measure because AI rarely creates value in isolation.

A model may summarise text, classify documents, predict risk, generate code, detect anomalies or recommend actions. But the value is realised only when the surrounding workflow changes. If the process stays the same, the organisation may simply insert AI into an old operating model and call it transformation.

That is not value realisation. That is tool adoption.

This is not a new problem. The history of information technology is full of periods where powerful technologies were visible everywhere except in the productivity statistics. Brynjolfsson, Rock and Syverson describe possible explanations for the modern productivity paradox: false hopes, mismeasurement, redistribution and implementation lags. They argue that implementation lags are likely an important part of the explanation.

The productivity J-Curve sharpens the point. New general-purpose technologies often require intangible investments before measurable productivity gains appear. Organisations must invest in process redesign, skills, data, management systems and complementary capabilities. During this phase, costs are visible, but benefits may not yet be fully measured. Later, when those intangible investments begin to pay off, productivity can accelerate.

The same logic applies to AI.

A bank may pay for AI infrastructure, cloud consumption, vendor tools, model development, data preparation, governance, training, change management and controls before the financial benefits become visible. If the measurement model looks only for immediate P&L impact, it may underestimate long-term value. If it accepts every efficiency claim without evidence, it may overstate value.

There is also a macroeconomic caution. Acemoglu’s 2024 analysis of AI starts from a task-based model and argues that aggregate macroeconomic effects may be more modest than large headline claims suggest. That does not contradict strong task-level evidence. It explains why task gains do not automatically translate into broad productivity gains without complementary organisational change.

The answer is not pessimism.

The answer is measurement discipline.

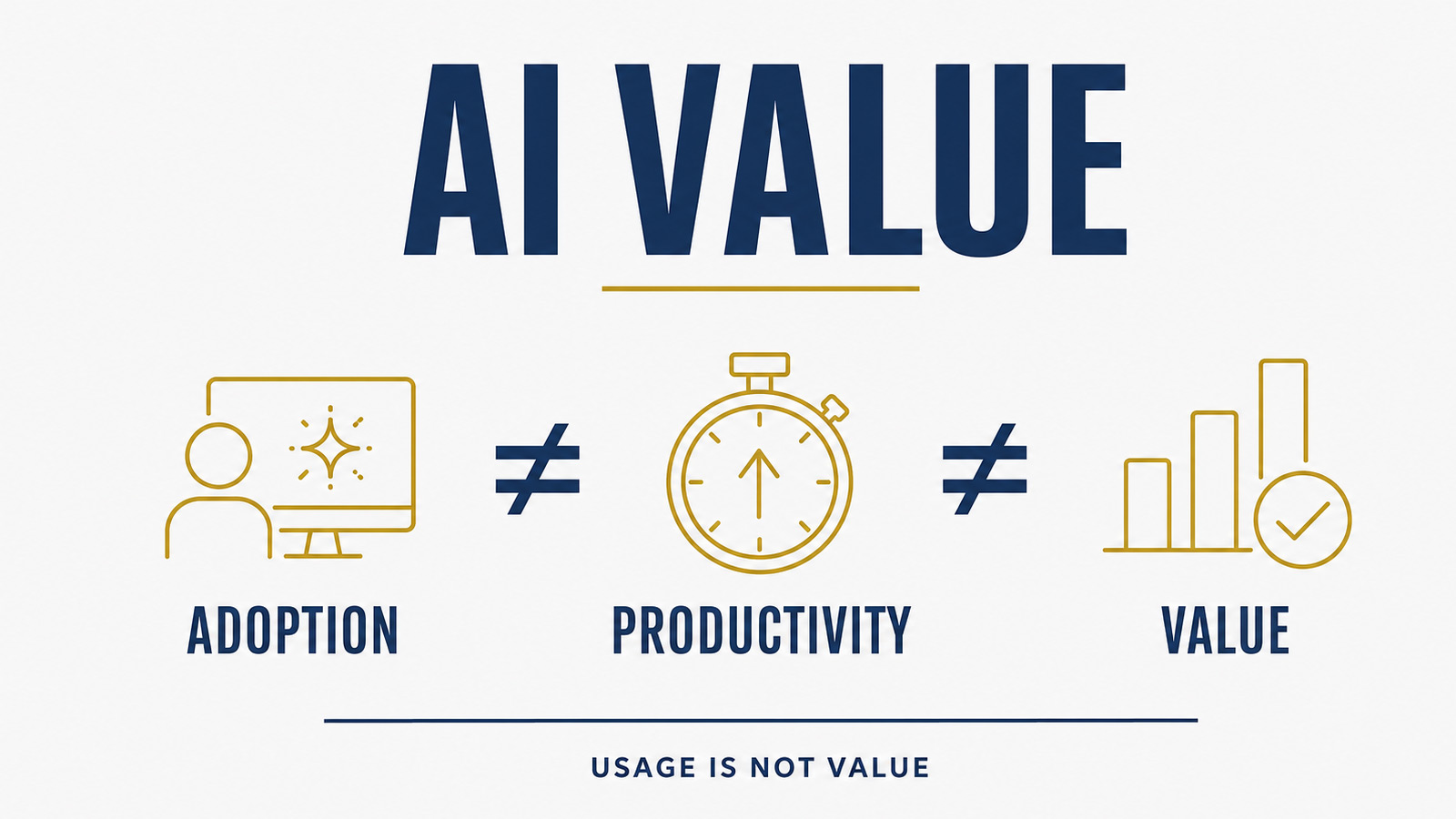

The First Rule: Separate Adoption, Productivity and Value

AI measurement should start with three separate concepts.

Adoption means that people or systems are using AI.

Productivity means that a task, activity or process is completed with less time, better quality, lower cost or higher throughput.

Business value means that productivity translates into an outcome that matters to the enterprise.

These three layers are related, but they are not the same.

High adoption may produce little value if users apply AI to low-value tasks, duplicate work, create review burden or generate outputs that are not trusted. High productivity may still fail to create P&L impact if saved time is not redeployed, if bottlenecks sit elsewhere in the process or if quality issues create downstream remediation.

This is why measurement must follow a value chain:

AI capability → task outcome → workflow outcome → business outcome → financial or strategic value.

For example, a document-intelligence model may classify incoming documents faster. That is a task outcome. If the classification feeds a redesigned onboarding workflow, it may reduce cycle time. That is a workflow outcome. If onboarding becomes faster without increasing risk, the business may improve customer conversion, capacity utilisation or service quality. That is business value.

The measurement question is therefore not “Did the model work?”

It is “Did the model change the process outcome that the business cares about?”

That distinction is the foundation of AI value governance.

The Evidence Is Real, but It Is Context-Specific

The best available evidence shows that AI can create large productivity gains in specific tasks. It also shows that the impact is highly context-dependent.

In writing tasks, Noy and Zhang found that access to ChatGPT reduced average completion time by 40% and improved output quality by 18%. That is strong task-level evidence, but it applies to a specific type of professional writing task under experimental conditions.

In customer support, Brynjolfsson, Li and Raymond studied the staggered introduction of a generative AI conversational assistant across 5,172 agents. They found a 15% average productivity increase, measured by issues resolved per hour, with stronger effects for less experienced and lower-skilled workers.

In software development, Peng, Kalliamvakou, Cihon and Demirer found that developers using GitHub Copilot completed a specific JavaScript programming task 55.8% faster than the control group.

At the same time, the evidence also warns against simple generalisation. Dell’Acqua and co-authors describe a “jagged technological frontier”: AI can improve performance for some tasks while worsening performance for others, even within similar knowledge-work settings.

METR’s 2025 study of experienced open-source developers provides an important corrective. In that setting, developers using early-2025 AI tools took 19% longer on assigned tasks in mature repositories where they had substantial prior experience. The authors describe this as a context-specific result, not a universal verdict on AI coding tools.

The lesson for executives is clear: AI value must be measured at the level of the task and the workflow. Generic productivity assumptions are not enough.

A use case should not inherit a benefit percentage from another organisation, another function or another study. It should define its own baseline, test population, measurement period, control group or counterfactual, and value logic.

A Practical AI Value Measurement Model

A useful AI value model should answer five questions.

- 1What business outcome should change?

- 2What workflow must change for that outcome to improve?

- 3What task-level improvement is AI expected to create?

- 4How will the organisation measure whether the change happened?

- 5What decision will be made if the value does not appear?

This creates a practical measurement model with five layers.

Layer One: Strategic Value

Strategic value describes why the use case matters. It connects AI to business priorities, not to technology enthusiasm.

Examples include faster onboarding, better risk detection, improved service quality, stronger operational resilience, better developer productivity, lower manual rework, improved control effectiveness or better knowledge reuse.

The strategic value statement should be short and testable.

Weak version: “Use AI to improve operations.”

Strong version: “Reduce manual document triage in onboarding by 30% while maintaining quality-control thresholds and auditability.”

The second version can be measured.

Layer Two: Baseline

A baseline is the current state before AI changes the process.

Without a baseline, every benefit claim is fragile.

A proper baseline should include current cycle time, cost per transaction, manual effort, error rate, rework, backlog, quality score, customer satisfaction, risk indicators, control exceptions and handover points where relevant.

The baseline must be measured before deployment, not reconstructed after success is claimed.

Layer Three: Task Effect

The task effect measures what AI changes directly.

This may be faster drafting, faster classification, faster coding, faster summarisation, better extraction accuracy, improved anomaly prioritisation or reduced search time.

Task effects are important because they are closest to the AI capability. But they are not sufficient. A 40% faster task does not automatically produce a 40% cheaper process.

The task may not be the bottleneck. The saved time may not be redeployed. Review burden may increase. Quality may vary. Downstream functions may still operate at the old pace.

Task-level measurement is necessary. It is not the full answer.

Layer Four: Workflow Effect

The workflow effect measures whether the process changed.

This is often where AI value is won or lost.

A good workflow measure may track end-to-end cycle time, number of handoffs, first-time-right rate, manual touches, exception queues, decision latency, rework loops, backlog ageing or control review effort.

This layer is also where workflow redesign becomes critical. McKinsey’s 2025 State of AI research found that 39% of respondents reported some level of enterprise-wide EBIT impact from AI, while most of those respondents attributed less than 5% of EBIT to AI. The same report defines AI high performers as respondents attributing at least 5% EBIT impact to AI and reporting significant value; this group represented about 6% of respondents. It also found that high performers were more likely to redesign workflows and that workflow redesign made one of the strongest contributions to meaningful business impact among the factors tested.

That finding fits the J-Curve logic. AI does not create enterprise value merely by being available. It creates value when the organisation changes how work is performed.

Layer Five: Enterprise Value

Enterprise value is the final outcome.

It may be financial, operational, customer-related, risk-related or strategic.

Financial value may include cost reduction, avoided cost, revenue uplift, margin improvement, reduced external spend or better capital efficiency. Operational value may include faster throughput, higher capacity, shorter queues or lower rework. Customer value may include faster response, higher satisfaction or improved availability. Risk value may include fewer control breaks, better detection, lower operational loss or stronger evidence. Strategic value may include faster product delivery, better decision quality or stronger organisational learning.

Not every AI use case needs direct revenue attribution. But every AI use case needs a value category.

If the value category is unclear, the use case is not ready for scale.

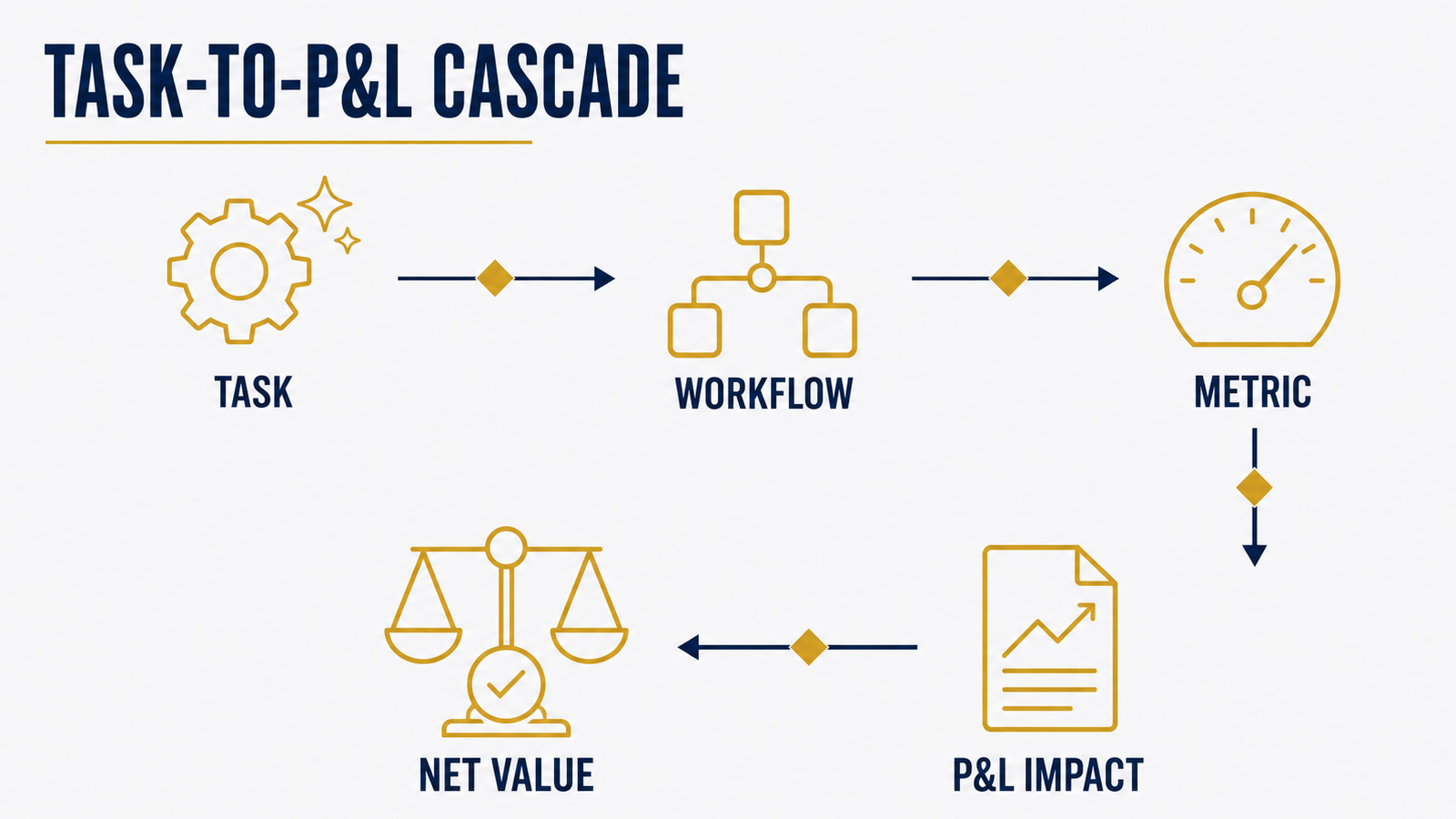

The Task-to-P&L Cascade

The Task-to-P&L Cascade is the five-layer model in motion.

It forces the organisation to connect model-level performance to business value for a specific use case.

A simple cascade looks like this:

1. AI improves a task.

2. The improved task changes a workflow.

3. The workflow change improves a business metric.

4. The business metric affects cost, revenue, risk, capital, customer experience or strategic capacity.

5. The impact is measured against baseline and compared with total cost of ownership.

This prevents two common mistakes.

The first mistake is stopping at model performance. A model can have strong accuracy and still create no business value if it does not change a process outcome.

The second mistake is jumping directly to financial benefit. A business case that claims cost savings without showing the task and workflow bridge is usually too weak for executive decision-making.

For example:

AI capability: A model summarises customer-service interactions.

Task effect: Agents spend less time reading case histories.

Workflow effect: Average handling time falls and first-contact resolution improves.

Business outcome: More cases are resolved per hour with stable quality.

Enterprise value: Capacity increases, backlog falls, customer satisfaction improves or cost-to-serve decreases.

The cascade makes the value logic auditable.

That is why it is particularly useful in banking. It supports management discipline without turning AI value measurement into a pure compliance exercise.

Why Workflow Redesign Is the Value Multiplier

AI often improves tasks before it improves processes.

That is why workflow redesign matters.

If AI makes one step faster but the rest of the workflow remains unchanged, the gain may disappear. The bottleneck may move. The queue may shift to a human reviewer. A control function may need more time to review AI-generated output. A business owner may not trust the result. A customer-facing process may still wait for approvals that AI does not affect.

This is how task productivity becomes trapped.

Workflow redesign asks a different question:

If AI changes what is possible, how should the process now operate?

That may involve removing unnecessary handoffs, changing review thresholds, redesigning exception management, adjusting role responsibilities, creating new quality checks, changing approval logic, improving data capture or redefining service-level expectations.

This is not technology implementation. It is operating-model design.

The strongest AI business cases will therefore include two plans: a technology plan and a workflow plan.

The technology plan explains the model, tool, data, architecture and controls.

The workflow plan explains how work changes, who does what, which steps disappear, which controls remain, where human judgement is required and how value will be measured.

Without the workflow plan, the value case is incomplete.

Total Cost of Ownership Must Be Real

AI business value cannot be measured only against licence cost.

The total cost of ownership is broader.

It may include infrastructure, cloud consumption, model access, vendor fees, internal engineering, data preparation, data quality remediation, integration, testing, validation, monitoring, user training, change management, control design, legal review, information security, privacy review, operational support, auditability and incident handling.

For generative AI, cost may also include prompt management, guardrails, retrieval infrastructure, knowledge-base maintenance, human review, output testing, content evaluation and model-risk documentation.

The cost side should also include opportunity cost. Senior management time, scarce engineering capacity and business change capacity are not free.

This is why AI value measurement should use a net-value view:

Gross benefit minus total cost of ownership minus risk-adjustment cost equals net value.

The risk-adjustment cost is important. A use case that creates efficiency but requires heavy review, remediation, manual correction or control effort may have a lower net value than the initial business case suggests.

This is not an argument against AI.

It is an argument for serious measurement.

Risk Value Is Business Value

In banking, business value is not only revenue or cost.

Risk value matters.

An AI system may create value by improving fraud detection, reducing false positives, enhancing monitoring, prioritising alerts, improving data quality, strengthening controls, reducing operational errors or supporting regulatory evidence. These outcomes may not always appear as immediate revenue. But they can be economically meaningful.

The ECB’s Financial Stability Review notes that AI could enhance risk-management capabilities, including more accurate risk assessment and predictions and more efficient capital and liquidity planning, while also recognising that benefits depend on how challenges around data, model development and deployment are addressed.

The BIS also frames AI in finance through key financial-system functions such as intermediation, insurance, asset management and payments, while analysing implications for financial stability and prudential policy.

This matters for value measurement. A bank should not force every AI use case into a narrow cost-saving model. Some AI use cases create value by improving decisions, controls or resilience.

Examples of risk-value metrics include:

- reduction in false negatives;

- reduction in false positives without lower detection quality;

- faster alert triage;

- improved case prioritisation;

- fewer manual control breaks;

- improved completeness of evidence;

- shorter incident-analysis time;

- better model monitoring;

- improved data-quality remediation;

- stronger audit trail.

Risk value should still be measured. It should not be treated as a vague qualitative benefit.

AI Value in Banking: The Right Unit of Measurement

For banks, the right unit of measurement is often not the model. It is the business service or workflow.

AI models do not create value in abstraction. They create value inside lending, onboarding, payments, operations, compliance, technology delivery, customer service, treasury, risk management, financial crime, reporting or software engineering.

The EBA has observed rising AI use in EU banking and payments. Its 2025 material states that 92% of EU banks are currently deploying AI and that 8% are pilot testing or discussing AI use cases.

That makes value measurement more important, not less.

As AI becomes more common, the differentiator is no longer whether an institution has AI. The differentiator is whether it can turn AI into measured, governed and scalable business outcomes.

A useful bank-level AI value taxonomy may include five categories.

Productivity Value

AI reduces time, effort or manual work.

Examples: drafting, summarisation, coding assistance, document triage, case preparation, knowledge search.

Quality Value

AI improves accuracy, consistency or completeness.

Examples: better classification, fewer missing fields, better evidence packs, improved documentation quality.

Risk Value

AI improves detection, monitoring, control or resilience.

Examples: fraud analytics, alert prioritisation, anomaly detection, control testing, operational-risk insight.

Customer Value

AI improves speed, personalisation, clarity or availability.

Examples: faster onboarding, better customer response, improved service routing, more consistent communication.

Strategic Capacity Value

AI increases the organisation’s ability to execute.

Examples: faster product development, better knowledge reuse, improved decision support, higher change capacity.

This taxonomy prevents the value discussion from becoming too narrow.

The Role of Finance

Finance should be involved early.

AI value measurement often fails when Finance is brought in only at the end to validate benefits that have already been claimed. The better model is to involve Finance before deployment, when baselines, benefit logic, cost categories and measurement periods are defined.

Finance should help distinguish between hard savings, soft savings, avoided cost, capacity release, productivity gain, risk reduction and revenue effect.

These categories should not be mixed.

A productivity gain becomes a hard saving only if the organisation can reduce cost, avoid planned hiring, increase throughput with the same capacity, reduce external spend or redeploy capacity into measurable higher-value work.

Saved minutes are not automatically saved money.

This point is essential. If AI saves employees time but the organisation does not know what happens to that time, the value case remains incomplete.

Finance should therefore require a capacity-redeployment logic:

- What time is saved?

- Where is it captured?

- Who owns it?

- How is it redeployed?

- Does it reduce cost, avoid cost, increase throughput, improve quality or support growth?

- How will that be measured?

This moves AI value from enthusiasm to management accounting.

The Role of Risk and Control Functions

Risk and control functions should not be treated as blockers in AI value measurement. They are part of the value system.

They help define whether the value is sustainable.

A use case that produces short-term efficiency but creates data risk, model risk, conduct risk, privacy risk, cyber risk, outsourcing risk or operational risk may not be a good value case. Conversely, a use case that strengthens control quality may create value even if it does not directly reduce headcount or increase revenue.

Risk and control functions should help define:

- acceptable use;

- risk appetite;

- model criticality;

- evidence requirements;

- human oversight;

- data lineage;

- monitoring expectations;

- exception handling;

- auditability;

- kill criteria.

This is how value measurement becomes credible.

The goal is not to slow down AI. The goal is to avoid measuring value in a way that ignores the cost of control.

A good AI value model includes control by design.

Kill Criteria Are Part of Value Governance

Every AI use case should have kill criteria.

This does not mean organisations should be negative. It means they should be disciplined.

A use case should be stopped, redesigned or kept in pilot if it does not meet agreed thresholds. Those thresholds may relate to business value, quality, adoption, risk, cost, explainability, user trust, operational fit or control evidence.

Examples of kill criteria include:

- no measurable workflow improvement after a defined period;

- benefits below agreed threshold;

- high manual review burden;

- poor user adoption after training and workflow redesign;

- unacceptable error profile;

- unstable model performance;

- unresolved data-quality issues;

- excessive total cost of ownership;

- inability to evidence control;

- better performance from a simpler solution.

Kill criteria are not a sign of failure.

They are a sign of mature capital allocation.

In AI, the opportunity cost of weak use cases is high. Every low-value use case consumes attention, data, engineering capacity, governance capacity and change capacity that could be used elsewhere.

A bank does not need every AI idea to scale.

It needs a disciplined way to decide which ones should.

A Board-Level AI Value Dashboard

Boards do not need a model-by-model technical report.

They need a value dashboard.

A useful AI value dashboard should show:

- number of AI use cases by value category;

- use cases in pilot, production and scale;

- baseline established or missing;

- measured task-level impact;

- measured workflow impact;

- financial value realised;

- risk or control value realised;

- total cost of ownership;

- adoption and active usage;

- quality and error indicators;

- human oversight metrics;

- open issues;

- kill, pivot or scale decisions;

- benefits signed off by Finance;

- control status signed off by Risk or relevant control functions.

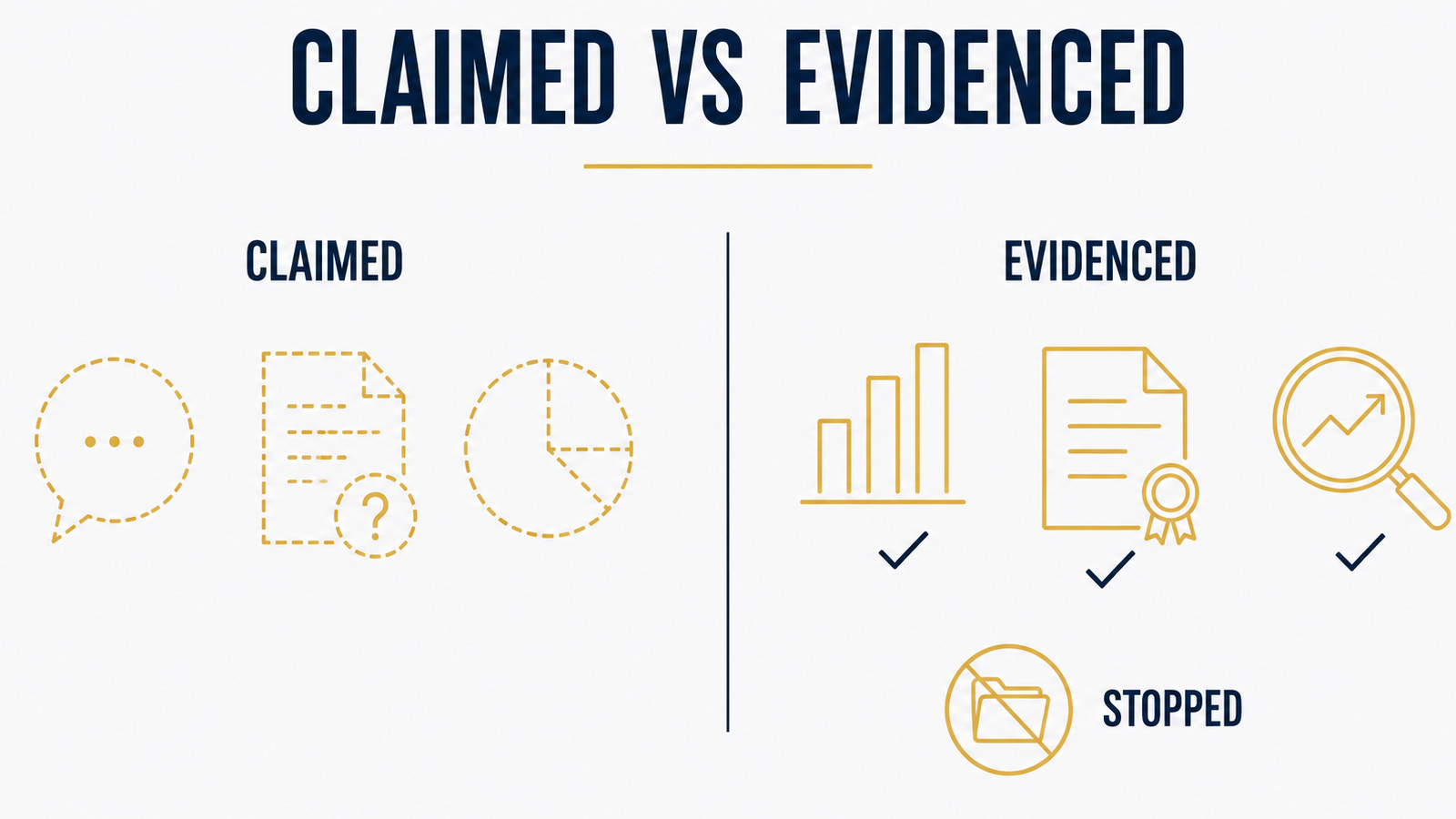

The dashboard should separate claimed value from evidenced value.

This is critical.

A board should be able to see which AI use cases are generating measurable outcomes, which are still hypotheses, which require workflow redesign, and which should be stopped.

The most important column in the dashboard may be simple:

“What decision is required?”

Scale, hold, redesign, stop or monitor.

That turns AI reporting into governance.

The AI Business Value Operating Model

To measure AI business value consistently, organisations need an operating model.

A practical model has seven components.

1. Value Thesis

Each use case starts with a clear statement of expected value.

2. Baseline

The current process outcome is measured before deployment.

3. Ownership

A business owner, technology owner, data owner and value owner are assigned.

4. Measurement Design

The organisation defines how value will be measured: before-and-after, A/B test, control group, phased rollout, matched comparison, time-and-motion study or operational metric tracking.

5. Workflow Redesign

The process is redesigned so that task-level productivity can become workflow-level value.

6. Control by Design

Risk, compliance, data protection, cyber, model risk and operational control requirements are built into the value model.

7. Decision Cadence

A governance forum reviews evidence and decides whether to scale, redesign, stop or continue.

This operating model is simple enough to use and strong enough to survive executive scrutiny.

What Executives Should Ask

Executives should ask fewer generic AI questions and more value questions.

Not: “How many AI pilots do we have?”

But:

- Which business outcomes are we trying to improve?

- Which workflows are being redesigned?

- Do we have a baseline before deployment?

- What is the task-level effect?

- What is the workflow-level effect?

- What is the enterprise-value effect?

- Has Finance validated the benefit logic?

- Have Risk and control functions validated the control logic?

- What is the total cost of ownership?

- Where are we seeing measurable value?

- Where are we only seeing usage?

- Which use cases should be scaled?

- Which should be stopped?

The questions themselves create the management discipline.

Conclusion: AI Value Is a Management Discipline

The central question is not whether AI can create value. It can.

The evidence is already strong in specific tasks: writing, customer support, coding, summarisation, knowledge work and selected analytical workflows. But the evidence is also clear that AI value is uneven, context-specific and dependent on workflow redesign. The same technology can accelerate one task, slow down another and create no enterprise value if the surrounding operating model does not change.

That is why measuring AI business value is not a reporting exercise. It is a management discipline.

It requires baselines before deployment, clear value hypotheses, task-level measurement, workflow-level measurement, Finance validation, risk-adjusted cost, control by design, kill criteria and board-level decision-making.

The best organisations will not be those with the longest list of AI pilots.

They will be those that can answer a harder question:

Where is AI changing measurable business outcomes, and can we prove it?

That is the standard for AI value.

And it is the standard that turns AI from experimentation into execution.